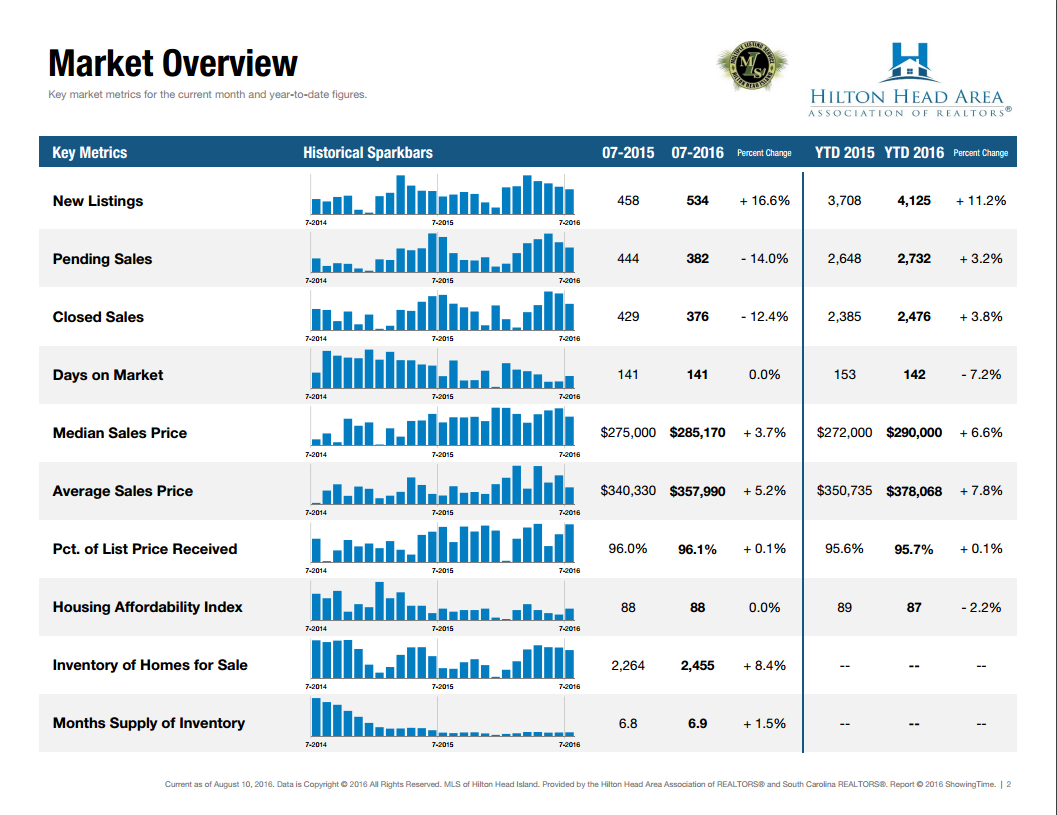

July 2016Even as prices rise in many communities, homes are selling faster now than they have in the past several years. This creates a situation where buyers need to move fast in order to secure homes, and they may have to pay more for them. While increasing prices generally coax more selling activity, there has been some hesitancy among potential sellers who worry that they will not be able to buy a desirable and reasonably priced home once they sell. New Listings were up 16.6 percent to 534. Pending Sales decreased 14.0 percent to 382. Inventory grew 8.4 percent to 2,455 units. Prices moved higher as Median Sales Price was up 3.7 percent to $285,170. Days on Market held steady at 141. Months Supply of Inventory was up 1.5 percent to 6.9 months, indicating that supply increased relative to demand. Low housing supply has already prevented an outright national boon in sales activity, despite a continuation of near record-low mortgage rates and an unemployment rate under 5.0 percent deep into 2016. The issue is not purchasing power. Many areas are falling behind last year’s closed sales totals simply because of lack of available inventory. As this continues, higher prices may put a deeper squeeze on the current buyer pool.

Click here to review the full Hilton Head Market Report July 2016 |

May 2016We are in the thick of an exciting period of home buying and selling, often with quick multiple offers that are near, at or even above asking price, depending on the factors of the home and submarket in question. It was widely predicted that we would see healthy sales activity during the second quarter of 2016, and the market has not disappointed. New Listings were up 15.4 percent to 599. Pending Sales increased 29.2 percent to 487. Inventory shrank 1.7 percent to 2,443 units. Prices moved higher as Median Sales Price was up 6.9 percent to $297,500. Days on Market decreased 10.5 percent to 136 days. Months Supply of Inventory was down 17.5 percent to 6.6 months, indicating that demand increased relative to supply. Although inventory is still being stretched thin in many areas, low mortgage rates coupled with higher wages have built a relatively sturdy housing marketplace. How long that can continue without fresh supply remains an important question, but conditions are seemingly good enough for serious buyers. With the current slow state of new construction for non-rental households, the road ahead could be tricky if demand remains high.

Click here to review the full Hilton Head Market Report May 2016 |

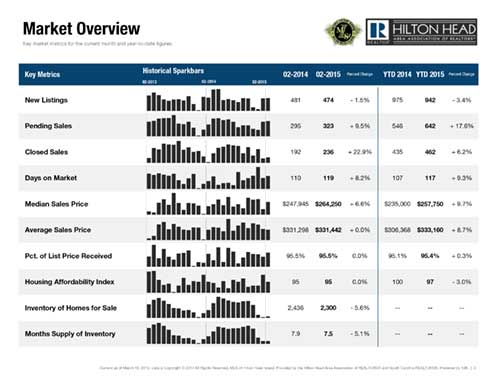

February 2015

Prices increased and Median Sales Price was up 6.6 percent to $264,250. Days on Market increased 8.2 percent to 119 days. Months Supply of Inventory was down 5.1 percent to 7.5 months, indicating that demand increased relative to supply. Click here to review the full Hilton Head Market Report Feb 2015 |

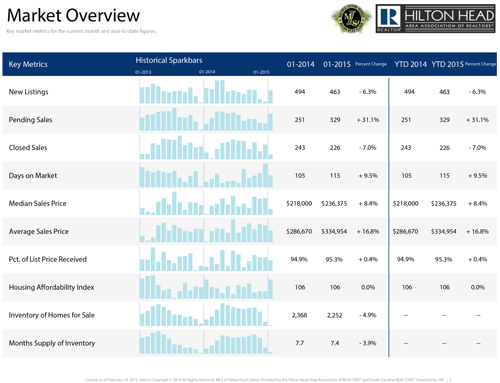

January 2015

There was a decrease in new listings of 6.3% since January of 2014, and 7% decrease in closed sales. Pending sales were up 31%. Average days on market has also increased by ten days, to 115, which is a 9.5% increase. Median sales price and average sales price have increased by 8.4% and 16.8%, respectively, resulting in a median sales price of $236,375 and an average sales price of $334,954. The percent of list price received has risen to 95.3%, a slight but notable 0.4% increase from this time last year. Inventory of homes for sale and the months supply of inventory are both decreasing, with a 4.9% change to inventory of homes for sale and a 3.9% change to the months supply of inventory. Click here to review the full Hilton Head Market Report Jan 2015 |

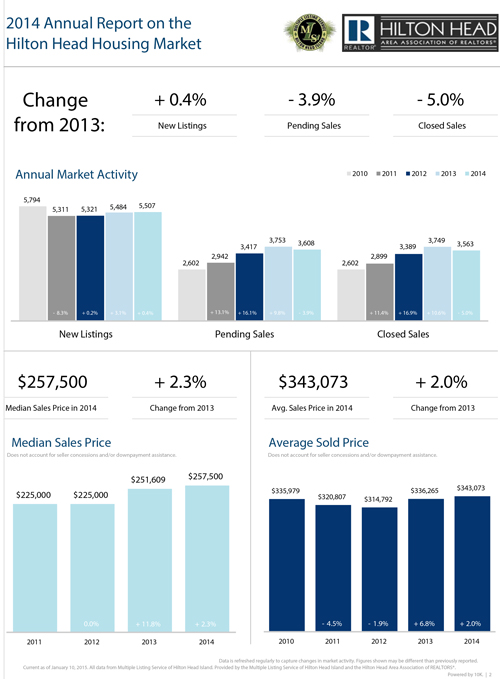

2014 Year in Review

The Hilton Head housing market has experienced many changes since 2013. Annual market activity has seen an overall decline, but the number of new listings has increased by 0.4%. The number of closed sales had the sharpest decline this year, down 5% from last. Pending sales followed fairly close behind with a decrease of 3.9%. Both median sales price and average sold price have increased, the former by 2.3% and the latter by 2%. The median sales price was 257,500, and the average sold price was greater, at $343,073. Houses have spent fewer days on the market since 2013, with the average being 113 days total. Months supply had a positive 4.1% change from 2013, and the inventory of homes for sale rose slightly to 2,287, increasing 0.2%. Percent of original price is steady at 95.4%. Click here to review the full 2014 Hilton Head Island MLS report |

January 2015 has displayed some improvements since January of last year. Median sales price is up 8.4% and average sales price is up 16.8%. There are over 30% more pending sales, but fewer new listings and fewer closed sales. The total percent of list price received has also increased, although only slightly at 0.4%.

January 2015 has displayed some improvements since January of last year. Median sales price is up 8.4% and average sales price is up 16.8%. There are over 30% more pending sales, but fewer new listings and fewer closed sales. The total percent of list price received has also increased, although only slightly at 0.4%.